EPF Explained: How our Provident Fund Builds our Retirement Corpus

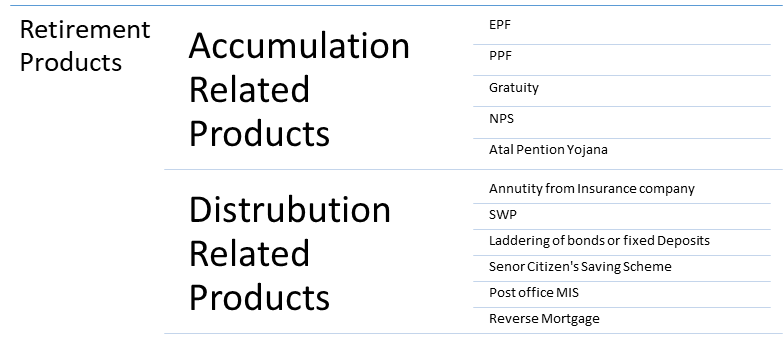

Retirement Products –

The retirement products can be categorized into two parts –

· Accumulation related products

· Distribution related products

Accumulation Related Products –

Accumulation related products are the products which helps us in generating retirement corpus. Some of the products mentioned above are mandatory in nature while others are voluntary.

EPF (Employees Provident Fund) –

EPF generally called PF (Provident Fund) is a mandatory saving cum investment scheme for the employees of an eligible company. The objective of this fund is to accumulate the retirement corpus. According to EPF norms the employee has to contribute the 12% of his basic pay and dearness allowance every month and the same amount will be contributed by the employer. The interest over the amount will be calculated on annual basis. Employee can withdraw all the amount accumulated in their EPF account at their retirement, but premature withdrawal is also available with certain conditions.

Some notable points in EPF contribution –

1. Employee’s Contribution = 12% of Basic pay + Dearness Allowance

Women employees can make the contribution of 8% rather than of 12% towards their EPF; this benefit is only available for the first three years of employment. It is done to promote the women's workforce in India.

2. Employer contribution = 12% of employee’s salary

Employer EPF contribution can be 10% of Employee’s salary if certain conditions are fulfilled –

· If the company has less than 20 employees

· The company incurs losses more than its entire net worth

· If the business is associated with beedi, jute, brick, guar gum or coir industry

3. An employee can contribute more than 12% towards their PF account, which is called a voluntary provident fund.

Interest Rate -

The interest rates on EPF are decided by the central board of trustees of EPFO (Employee Provident Fund Organisation). The ministry of finance reviews and approves the proposed rate given by the central board of trustees.

If the employee does not make any contribution for the three years consecutively, the account becomes dormant or inactive. Once the account becomes inoperative, then he will not get any interest over their accumulated fund. After 7 years of being inoperative, the money of this account transferred to the senior citizen welfare fund if there is no claim received.

Withdrawal –

The employee becomes eligible for the pension after the age of 58 and can withdraw their amount fully or partially. An employee can withdraw the full amount in some cases.

· When the employee retires

· When the employee remains unemployed for more than 2 months.

Employee can withdraw their amount partially with certain conditions –

· For medical – The employee can withdraw 6 months of basic salary plus dearness allowance or the total employee’s share, whichever is lower. For medical purposes there is no need to fulfil minimum years of service required.

· For marriage – An employee can withdraw up to 50% of the employee's share of contribution to EPF with interest. For this withdrawal employee need to fulfil 7 years of service.

· For education – For educational purposes an employee can withdraw Up to 50% of the employee's share of contribution to EPF with interest. For this he needs to complete 7 years of service.

· For home loan repayment – An employee can withdraw up to 36 months’ basic salary plus dearness allowance or Total corpus consisting of the employer's and employee’s contributions with interest or Total outstanding principal and interest on a housing loan, whichever is lower among these. For this employee need to fulfil minimum 10 years of service.

· For home renovation – An employee can withdraw Up to 12 months’ basic wages and dearness allowance or employees' contribution with interest or total cost, whichever is lower.

Tax implications –

The contributions made by the employee to EPF are eligible for deduction under section 80C along with other investments/expenses mentioned in that section but if the annual contributions of more than 2.5 lakh including Voluntary Provident fund account, the interest earned on these is taxable.

Tax on withdrawal –

EPF withdrawal is tax – free but there are some exceptions –

1. Withdrawal before five years –

If the employee does not complete its five-year service consecutively than the amount withdrawn is taxable in his hand. But the amount may be tax-free in following cases –

· If the employment is terminated due to an employee’s ill health or the employer has discontinued its business or any other reason for withdrawal, which is beyond the control of the employee.

· If the employee changes his employer in less than five years, then the employee can transfer his PF account balance of the existing employer to the new employer.

2. After five years –

If the employee has completed five years of service consecutively than the amount withdrawn in his hand is tax-free.

Today we have understood about the EPF (Employee Provident Fund) in later post we will cover other accumulation related products.